132. The Dominion of Incumbents

“Software is Feeding the World” is a weekly newsletter about technology trends for Food/AgTech leaders.

Greetings from the San Francisco Bay Area. I will be at the World Agritech Summit in San Francisco on the 14th and 15th of March. If you are going to be there, it would be great to meet in person.

As we head to the World Agritech Summit in San Francisco, where hundreds of Agtech companies, including incumbents will gather to discuss problems, use cases, collaborations, business models, and new technology which can move agriculture to a better spot, it is good to reflect on what factors can really drive change in an industry dominated by incumbents.

The dominion of incumbents

A few months ago, I met a farmer from France. He was a 16th generation farmer on more or less the same piece of land. My mind was blown!

If you assume 25 years as one generation, the family has farmed there for roughly 400 years. The farm and the family have survived Louis the XIV, the French Revolution (!!!), Napoleon (!!!), and two World Wars (!!!!).

There are very few professions outside of farming, where the number of generations for which your family has been farming is portrayed as a strength.

Incumbency translates to experience, and experience to expertise. This is very much related to the land asset which has been held in the family for many generations.

Incumbency is a huge challenge in politics. Political dynasties are frowned upon by people who are not part of the dynasty.

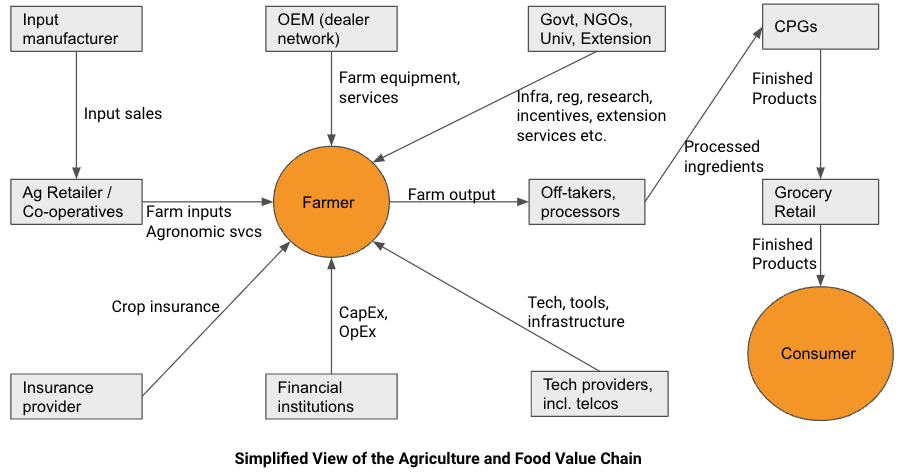

Within the broader agriculture ecosystem, incumbency is considered a strength. Incumbents control many assets, which are hard to build, and make it extremely difficult for new entrants to come into the market.

There is a significant concentration within the industry, along the entire food and agriculture value chain.

|

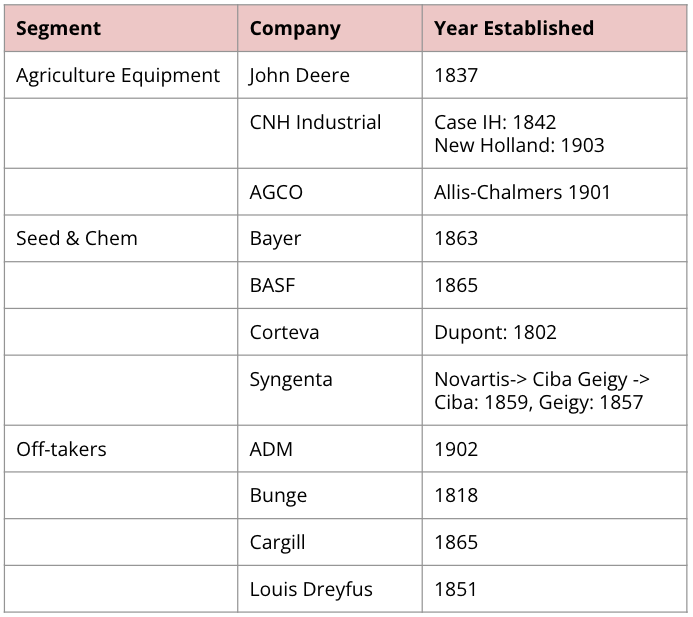

Between 3 to 5 organizations control more than 60% of the business worldwide, whether it is seed or chemicals or equipment or off-takers or processors. Ariel Patton did a nice analysis in her post (Topsoil) and named companies which control more than 50% of the market in each segment in the US across the value chain.

|

Source: The soberting details behind the latest seed monopoly chart (Civil Eats) (2019)

The most important physical products for farming are inputs like seed and chemicals, and equipment like tractors, and harvesters. These companies have maintained an iron grip on the product portfolio, and most importantly the distribution channel for input products (especially in the global north).

Farmers also need to market their products, and it requires a physical infrastructure optimized for their product to move it from the farm to processing.

Due to a concentrated industry structure, there is limited space for startups to enter and bring innovation to the market. Concentrated industry structures often tend to stifle innovation, which is not great for the industry.

What is even more interesting is to see how long these companies have been around.

|

The youngest company in this group is ADM (1902) and has survived and thrived for 121 years! If you look at other industries, the top companies in an industry change positions frequently. (Just compare the Forbes top 100 countries every 10 years since the list was published, and you will see many changes in the list every 10 years or so.)

Industries which require heavy infrastructure and developing strong physical supply chains are more resilient to anti-incumbency (for example, Tesla is the only new car company which has formed in the last few years, though given the large number of car manufacturers, there is a strong competition among the rest of them).

It is not easy to disrupt these incumbents from their dominion!

What drives change in an industry or provides an opening to others?

As Seana Day has reflected on her latest post,

Overall, the basic farm support structure has not changed much in the past decade. People still either sell ag products (e.g., machinery, equipment, inputs) or ag services (e.g., financial, insurance, custom farming) to farmers to help them run their business and bring their goods to market.

Typically there are four factors which can drive change in the industry.

1. Singular events or systemic shocks

If you think outside of agriculture, a 40 year old highly respected and trusted institution like the Silicon Valley Bank has gone up in flames in days. Lehman brothers famously crashed and burned within days and weeks, after being in business for 158 years!!

The COVID pandemic has ushered in massive changes in how we work, how we collaborate, and what we value. It led to a rise of remote work, telemedicine, and online shopping, though those trends have come back to pre-pandemic levels (except maybe remote work).

Within agriculture, what could be singular events or systemic shocks? Russia’s war on Ukraine has spiked fertilizer prices, but it probably has helped existing providers. It might help with more digitization as farmers try to optimize their input usage.

One potential event which could have a negative impact is a cyber attack on the infrastructure and assets of these companies, which creates a massive erosion of confidence in the brand. The likelihood of such an event is very low. (I had covered issues related to cybersecurity in edition 70. A tractorload of vulnerabilities)

When singular events or systemic shocks happen, large incumbents might be better able to weather the shocks, than say startups which can get wiped out. (Unless the singular event acts as a tailwind - for example, Zoom took off during the pandemic, but so did many of the large internet behemoths.)

2. Regulation or policy change

Regulation or policy change can sometimes upend an industry, and create space for new entrants to come into the market. In the US, the breakup of Ma Bell into Baby Bells in the 1980s led to a surge in competition for long distance services by companies like Sprint and MCI.

I experienced personally as the Indian government dismantled the old socialist state (to some extent) and opened up India markets for competition in 1991. It created a surge of entrepreneurship, created many new companies in many industries, and in general led to uplifting of many millions of Indians out of poverty.

The European Green Deal has spurred an interest in new technologies for reduction in chemical usage, transition to organic farming, etc., though the Ukraine war has dampened the enthusiasm for the Green Deal.

The immigration policies of the United States often create problems for growers for specialty crop as they are so labor dependent. Any changes in the immigration policy will drive a big change in the specialty crop industry.

Climate change and any regulation around climate change could be a potentially massive force which can drive change in the industry.

For example, any change to the current Renewable Fuel Standards, which ensure that most of the corn grown in the United States ends up as fuel, or animal feed, could have a huge impact on what farmers grow in the Midwest and in-turn to all the companies which service growing corn (input providers, equipment makers, off takers etc.). (Corn and ethanol were covered in great detail by my friend Sarah Mock and others on the AEI podcast series Corn Saves America - Season 2)

Typically, large incumbents are able to bear the cost of increased regulation much more efficiently compared to a startup, as the compliance costs are spread across a larger revenue base. Due to this, you will often see incumbents push for regulation for the industry, as they know that even if regulations are costly to them, they are much costlier to upstarts and new entrants to the market.

3. Consumer trends

Consumer trends have and will continue to have a direct impact on the food and agriculture industry, but it remains to be seen if it will actually upend the existing structure of the industry. Current consumer trends point towards a desire for more sustainable products or food grown in a sustainable or humane fashion (in the case of animal products).

Most big incumbents have already made pledges for net zero or some percentage reduction in GHG by a certain date. Agfunder News has been keeping track of these pledges, and the number of pledges have snowballed over the last few years.

The question is if this trend will disrupt any of the existing incumbents. I don’t believe it will have a huge impact on input, equipment, or offtake incumbents. This will open up space for new CPGs, and grocery retailers who can provide newer and more sustainable (whatever that means) products to consumers.

In fact, in early 2022, German think tank NewClimate “took 25 of the world’s major corporations to task and found that most are committing to less than they declare in the news.”

|

According to a report from Common Dreams, “Big Ag Exploiting Carbon Markets to Intensify Grip on Food System”

The criticism in the report is extended to say that the use of digital agriculture platforms drives more users to their digital solutions and further incentivizes and promotes their products.

It remains to be seen if consumer preferences drive any change in incumbents.

4. Technology and business model change

Technology is obviously a big driver of change brought about by smaller nimble companies, which can end up disrupting incumbents. There are many such examples in the last few years. Social media and the business model around social media pushed many magazines and newspapers into oblivion.

Uber famously cobbled together different pieces, but with an eye on technology and had a huge impact on the transportation industry.

Within agriculture RoundUp Ready soybean was a technologically genius move, and more so from a business standpoint.

Within agriculture, and Agtech, startups with bold and new ideas will have some chance to take on the incumbents. It will be extremely difficult as incumbents still control all the distribution channels for new products, and market access for the finished product.

As Alex Rampell of a16z very famously said,

Within commodity row crops, the markets in the US are thin (narrow) Markets. Due to this even if a new market entrant was able to capture some early customers, it is very difficult for them to scale. Their best form of exit is an acquisition by an existing company or merge with another small company to become an attractive target for an incumbent.

There are some interesting technology trends, which could potentially create some massive change in the industry. For example, this newsletter has often talked about data and machine learning. Here are some opportunities Seana Day talks about in her blog post,

- The aggregation of trillions of data points is leading to an unprecedented understanding of risk, pricing, and value but the development of a skilled workforce to provide context and insight continues to lag, even current demand

- A rapidly aging professional and office workforce for which little has been done to transfer knowledge

- The cost and complexity of maintaining legacy systems and technical debt will continue to stymie progress

- Siloed data across ag value chains will continue to lead to limited visibility into cost drivers and missed revenue opportunities.

There are many other technological wedges for agriculture startups to work on. Here are some examples, (not a comprehensive list)

- CRISPR

- Fully automatic agriculture equipment operating on the farm.

- Small size but a large number of smart equipment units operating seamlessly on the farm.

- Use of AI, ML, and large language models across a variety of user experiences, and problem sets.

- Effective alternatives for the current set of inputs, especially chemical inputs.

- MRV tools for tracking sustainability.

As I head to World Agritech next week, I will be looking out for startups, who have elegant yet powerful tech solutions to solve some of our most pressing problems.

Seana Day is quite hopeful about the power of tech and digitization of the industry.

Will they be working with incumbents or will they challenge the incumbents remains to be seen.

What do you think?

💗 If you like “Software is feeding the world”, please share with a friend.

🙏 If you don’t mind answering 3 questions anonymously (2 are optional), I would love to get your feedback.

About me

My name is Rhishi Pethe. I lead the product management and technology delivery teams at Mineral, an Alphabet company. The views expressed in this newsletter are my personal opinions.

Rhishi Pethe

Agriculture and Technology or AgTech

“Software is Feeding the World” is a weekly newsletter about technology trends for Food/AgTech leaders. Greetings from the San Francisco Bay Area after a long’ish break. Due to a technical issue, today’s edition is coming out later than normal. I hope to go back to normal operations starting from next week. Now onto this week’s edition. There has been significant talk about Large Language Models (LLMs) like Bard and ChatGPT recently. My friend Shane Thomas did a fantastic primer on the...

“Software is Feeding the World” is a weekly newsletter about technology trends for Food/AgTech leaders. Greetings from the San Francisco Bay Area. Interoperability is often on people’s minds when it comes to agriculture data. I have written about it over the past three years, and it is time to do a refresher again. Image source Potential problems with interoperability in agriculture data Interoperability in agriculture data refers to the ability of different agricultural systems and software...

“Software is Feeding the World” is a weekly newsletter about technology trends for Food/AgTech leaders. Greetings from the San Francisco Bay Area. The rain has taken a breather and hopefully is on its way out. My Work World Agritech San Francisco 2023 reflections World Agritech 2023 in San Francisco is behind us. I published some of my reflections from the event on my blog. I talk about my reasons to continue to go to the event, my 5 key takeaways from the event (independent voices matter,...